How much should you borrow?

If you’re running a business and you’ve reached a barrier – a chance to grow that requires capital, or a severe dip in your profits that needs a bail-out – you may feel you need to take out a loan. Before you rush off to the bank, stop and think about your financial situation first.

What will you use the money for?

If you’re thinking about buying new equipment or other assets that will enhance your business and boost profits, getting a loan could be a good idea. But borrowing to bail out your business isn’t always the best way to recover.

Can you trim expenses?

Whether you’re investing in new assets or trying to recoup some losses, this is an important exercise. Borrowing means repayments, so reducing other outgoings can help cover those, and could be one way to climb out of a hole.

Can you afford to borrow?

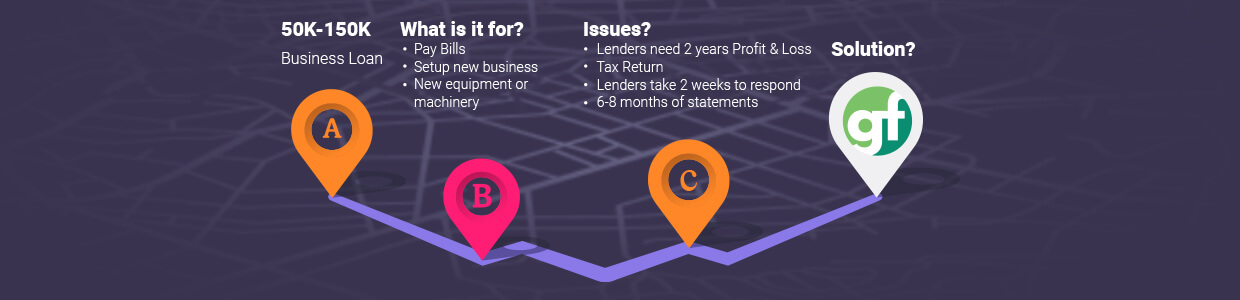

All businesses have highs and lows, times when profits are up as well as when bills flood in. Making loan repayments should be possible at all stages of your business, without the risk of defaulting. To be sure you can manage them, review your books from the last two years. This will help you get a cash flow forecast ready to reassure your lender – and yourself – that you can cope with repayments.

Don’t forget to factor interest

How much you pay in interest is dictated not just by the rate itself, but also by the term of your loan. A shorter-term will have higher repayments but will cost you less in interest, so you save money in the long run. Find out more by using a debt calculator. Enter different rates and terms to work out how much you can afford to repay.

How much do you need to borrow?

Once you’ve done all your homework, and you’ve decided to go ahead with a loan, it’s time to develop a business plan. Check out New Zealand Trade and Enterprise (NZTE) for a guide on how to do this. You’ll need it to work out how much you need to borrow and to support your case when you front up to a lender.

Any entity intending to lend you money will want to know all the details of your business – what you produce or offer, your future goals, and crucially, how you’ll spend your loan money. Of course, they also want to see your plan for repaying the loan. All this should be made clear in your business plan, along with exact costs of the assets you might be investing in, and how they will contribute to your business.

Get ready to make your pitch

You’ve answered all the questions, done your cashflow, and developed your business plan. Now you’re ready to approach lenders for that loan you need. But are you? Here are some tips to making that meeting go your way:

Be professional

Prepare a complete breakdown of your business in one sleek folder, including the previous two year’s accounts, financial projections, your business plan, and a concise executive summary that sets out your objectives and how you’ll use the lender’s money to realise them.

Sell yourself and your idea

You believe in yourself, and in the future success of your enterprise, so put any worries you have aside and go into the meeting ready to sell yourself and your plan for the development of your business. Let your enthusiasm be infectious.

Be ready to answer questions

Try to anticipate the questions your loan officer might ask and have the answers to hand. If there’s anything in your offering that needs explaining, they’ll notice and ask for more details. Answer with confidence – make your attitude set the tone for the meeting.

What kind of loan do you want?

Depending on the kind of business you’re running, choose the kind of loan that works best for you – fixed or floating.

Fixed – so you know your outgoings

A loan with a fixed interest rate has the same repayments for the whole term. Some businesses need this kind of stability, especially when other costs and incomes are variable.

Floating – to pay off faster

You might have windfalls from time to time in your business, and a floating rate means you can use some of them to pay down your loan faster without penalty. You can also change the repayment as needed, as long as you meet the minimum payment. You save on interest over the longer term, too.

Whatever you choose, be prepared to offer some kind of security – that might be either your commercial premises or your home.

Go for a broker

If all this high finance seems too much to cope with, but you still want to go ahead with your plans, talk to a mortgage broker. Not only will they help you with all the preparation and reporting, they’ll also shop around lenders for the best deal for you and manage repayments too. Be sure to choose a broker who is experienced in business lending and can advise you on options you may not have considered, keep you away from ‘too good to be true’ deals, and answer any questions you may have about financing your business. Not only will a broker save you time and stress, you’ll also have a fully experienced person going in to bat for you with lenders.

Fine Tuning the Details

Once you have the amount you want. Decided what it is you are after. Whether that be to pay for bills, to franchise your company, allocating capital for a new business start-up or purchasing new machinery it all comes down to your approach.

A $50,000-$150,000 cash injection to your small or medium-size business can go a long way with getting your finances back on track and working to grow your business at pace.

Growing your business? Be prepared

Sometimes your business needs a cash injection to help it get to the next level. When you have to borrow that money, it’s a good idea first to make sure you really need it, you can meet the repayments without endangering your enterprise, and you’re prepared to show lenders that you’re a good credit risk. A business plan and cash flow forecast are a must, so lenders can see clearly where their money will be spent.

Save yourself time and stress, and ensure you’ve covered all the bases, by enlisting the skills of an experienced broker. You’ll get help with preparation, and maybe even a better loan deal, with a broker on hand to negotiate for you.

Thinking of borrowing to expand your business? Talk to Global Finance for the best advice.